Elasticity

Definition of Elasticity: A measure of a variable's sensitivity to a change in another variable. In economics, elasticity refers the degree to which individuals (consumers/producers) change their demand/amount supplied in response to price or income changes.

Calculated as:

Elasticity is used to assess the change in consumer demand as a result of a change in the good's price. When the value is greater than 1, this suggests that the demand for the good/service is affected by the price, whereas a value that is less than 1 suggest that the demand is insensitive to price.

Price Elasticity Of Demand

Price elasticity of demand measures the responsiveness of demand to changes in price for a particular good. If the price elasticity of demand is equal to 0, demand is perfectly inelastic (i.e., demand does not change when price changes). Values between zero and one indicate that demand is inelastic (this occurs when the percent change in demand is less than the percent change in price). When price elasticity of demand equals one, demand is unit elastic (the percent change in demand is equal to the percent change in price). Finally, if the value is greater than one, demand is perfectly elastic (demand is affected to a greater degree by changes in price).

For example, if the quantity demanded for a good increases 15% in response to a 10% increase in price, the price elasticity of demand would be 15% / 10% = 1.5. The degree to which the quantity demanded for a good changes in response to a change in price can be influenced by a number of factors. Factors include the number of close substitutes (demand is more elastic if there are close substitutes) and whether the good is a necessity or luxury (necessities tend to have inelastic demand while luxuries are more elastic).

Businesses evaluate price elasticity of demand for various products to help predict the impact of a pricing on product sales. Typically, businesses charge higher prices if demand for the product is price inelastic.

For example, if the quantity demanded for a good increases 15% in response to a 10% increase in price, the price elasticity of demand would be 15% / 10% = 1.5. The degree to which the quantity demanded for a good changes in response to a change in price can be influenced by a number of factors. Factors include the number of close substitutes (demand is more elastic if there are close substitutes) and whether the good is a necessity or luxury (necessities tend to have inelastic demand while luxuries are more elastic).

Businesses evaluate price elasticity of demand for various products to help predict the impact of a pricing on product sales. Typically, businesses charge higher prices if demand for the product is price inelastic.

Cross Elasticity Of Demand

The cross elasticity of demand for substitute goods will always be positive, because the demand for one good will increase if the price for the other good increases. For example, if the price of coffee increases (but everything else stays the same), the quantity demanded for tea (a substitute beverage) will increase as consumers switch to an alternative.

On the other hand, the coefficient for compliments will be negative. For example, if the price of coffee increases (but everything else stays the same), the quantity demanded for coffee stir sticks will drop as consumers will purchase fewer sticks. If the coefficient is 0, then the two goods are not related.

On the other hand, the coefficient for compliments will be negative. For example, if the price of coffee increases (but everything else stays the same), the quantity demanded for coffee stir sticks will drop as consumers will purchase fewer sticks. If the coefficient is 0, then the two goods are not related.

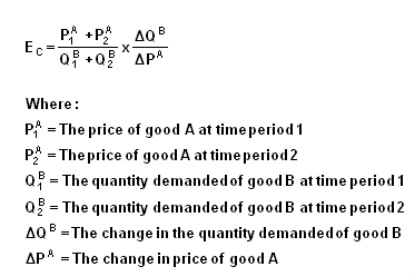

Cross elasticity of demand

Is an economic concept that measures the responsiveness in the quantity demand of one good when a change in price takes place in another good. The measure is calculated by taking the percentage change in the quantity demanded of one good, divided by the percentage change in price of the substitute good.